Along with the increase in online shopping, a new phenomenon exploded in popularity during the pandemic. Customers now have a new way to shop as a growing number of retailers embrace buy now, pay later (BNPL). BNPL plans are typically aimed at shoppers who impulse buy, typically purchasing fashion apparel or other small items. Shoppers who use BNPL are mainly Gen Z and Millennial shoppers who either don’t have or choose not to use credit cards. This option also makes a lot of sense for shoppers who don’t have the funds to cover the total purchase but will over the next several paychecks.

What Is Buy Now, Pay Later?

Buy now, pay later is a type of installment loan that lets customers make a purchase and receive it immediately but pay for it at a later time. It allows shoppers to divide their purchases into multiple equal payments, often interest-free, which can make even the biggest-ticket items seem affordable — and the smallest buys seem almost negligible. BNPL plans are similar to layaways but with BNPL, customers receive the product immediately.

Currently, buy now, pay later only makes up about 2% of all global payments. However, according to Bloomberg Intelligence, global sales volumes using BNPL are expected to double and could top $181 billion by 2022. As stated by Gartner, buy now, pay later adoption has surged, with major vendors Klarna, Affirm, and Afterpay reporting year-over-year volume growth rates of 46%, 83%, and 104%, respectively.

How Does Buy Now, Pay Later Work?

The “installment plan” is the historical precursor to today’s BNPL craze. This way of paying off purchases weekly or monthly evolved from 1840 onward, as manufacturers of furniture, pianos, and farm equipment looked to make their products more attainable. These days customers will more often come across buy now, pay later when shopping online at retailers like Target, Walmart, and Amazon.

Customers using buy now, pay later define a set of payments, then they pay that on a schedule. Usually, BNPL plans are interest and fee-free if the installments are paid on time. Sometimes providers may charge interest but typically this will allow customers to spend a larger amount with payments over a longer period of time.

Many buy now, pay later providers are not only introducing browser extensions, but apps as well, which lets customers use BNPL plans when shopping at brick-and-mortar stores, too. The colorful apps are attractively simple and typically involve only minimal (so-called “soft”) credit checks. At checkout, have the option to break up their total purchase and pay a smaller amount now, instead of the full balance.

The Main Drivers of the BNPL Trend for Millenials and Gen Z

Younger generations are enjoying the benefits of buy now, pay later in lieu of using traditional credit cards. It helps these consumers buy the clothing, make-up, and electronics they long for and helps them keep up with their peers. At the same time, these shoppers are looking to save money. However, there are other factors that drive them:

- Control: Millennials have been hit particularly hard by the economic environment, increasing the demand for flexible financial options. Therefore, similar to subscription-based services, BNPL solutions provide them with a greater sense of control and predictability.

- Sustainability: They are also driven by value and sustainability, so this type of payment vehicle allows them to buy fewer things of better quality, and spend more to buy less.

- Transparency: Buy now, pay later is often considered more straightforward than credit cards, which are seen as having hidden fees and confusing terms of agreement. This generation is used to subscriptions and paying monthly or weekly fees for all sorts of things. So breaking down payments into monthly costs is a familiar concept.

Antavo’s definitive guide assists you in designing, launching and managing a loyalty program that’s the perfect fit for your target audience.

Companies Embracing Buy Now, Pay Later

Many retailers have also become big fans of buy now, pay later, as these point-of-sale loans are easy for them to manage. Some of the largest BNPL solutions are partnering with retailers like Old Navy, PrettyLittleThing, ASOS, Sephora, and JD Sports. Offering BNPL tends to lead to bigger baskets and greater customer loyalty. According to a study, more than 49 percent of people spend more when using buy now, pay later than they would if paying by credit card.

Additional benefits that companies enjoy with BNPL include:

- Higher conversion: Buy now, pay later allows retailers to convert customers’ wishes into sales. Websites that offer these plans were able to convert a browser to a buyer 6% of the time versus 4% to websites that don’t.

- Increased average order value: Installment payments give customers options and convenience when it comes to managing budgets and purchasing. It also increases trust between retailers and shoppers, leading to incremental sales, higher average purchase sizes, and higher frequency of purchase.

- New customers: Attracting a customer that a retailer might not have been able to sway otherwise is yet another benefit of offering BNPL. Customers who otherwise wouldn’t have purchased an item due to its high price might change their minds if they can settle the payment in installments.

Buy Now, Pay Later Plans Enhanced By Loyalty Programs

Companies providing buy now, pay later have started augmenting their services with loyalty programs as well. When such providers decide to implement a rewards program, they basically have two options.

One option is to encourage purchases made with BNPL by giving customers points when they shop using their service. To do so, BNPL providers can offer members amazing perks like exclusive online and offline sales, or shopping experiences from world-class brands, such as Nike, Samsung, Starbucks, or Macy’s. Customers might even earn an extra layer of rewards if they are already part of an existing loyalty program through the retailer. These programs tend to evolve the shopping experience to deliver inspiration, convenience and even create a community.

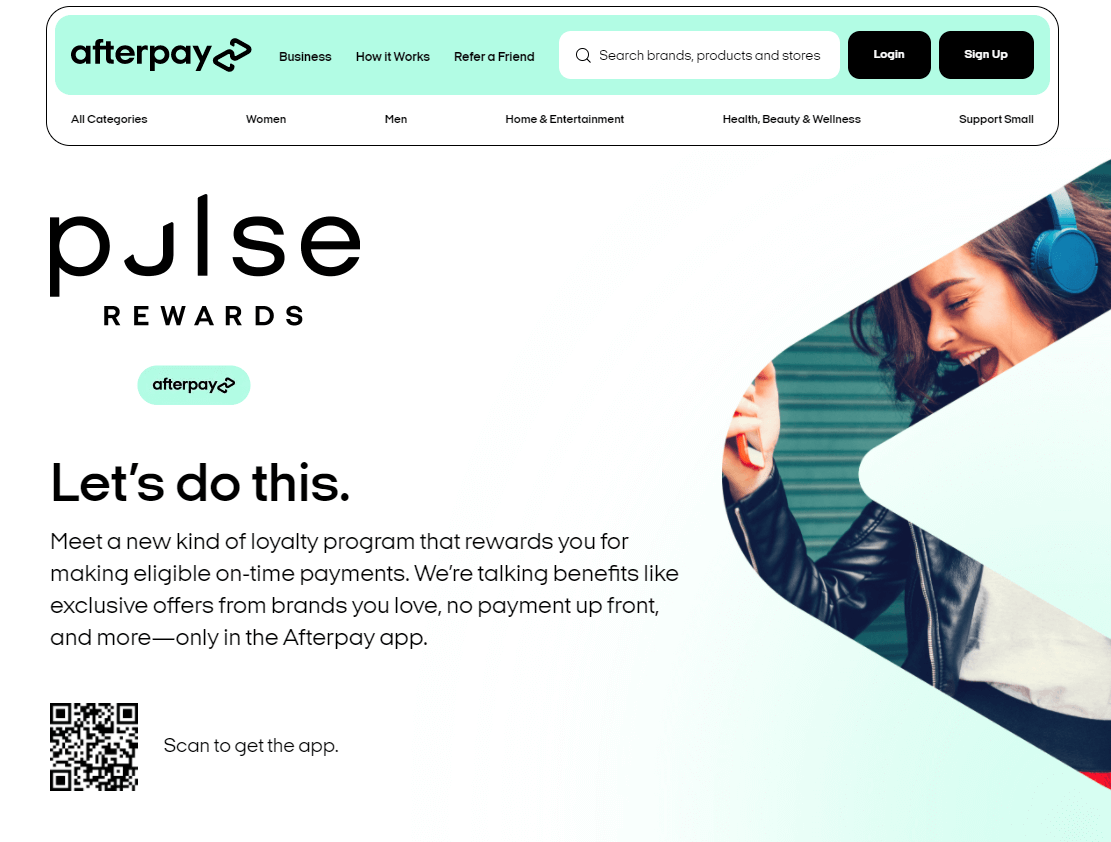

The other option is to reward responsible spending and eligible on-time payments. In order to encourage such behavior, members only earn points once their payments are completed and paid on schedule. Afterpay is one provider who does this with their loyalty program, Pulse Rewards. The loyalty program has three tiers: Gold, Platinum, and Mint, each with different benefits, such as welcome offers and a waiver of the up-ront payment requirement. The more points customers earn, the more tiers and exclusive rewards they can unlock.

Loyalty programs offered by deferred payment service providers usually offer customers more freedom in the rewards program and curated rewards without fees or high interest rates. They’ve chosen this structure because, based on feedback, customers often find traditional credit card loyalty memberships confusing and difficult to navigate.

How BNPL Is Changing the Loyalty Game for Financial Institutions

The increase in buy now, pay later installment payment services has also had an impact on financial institutions. It can motivate them to shift their strategy and offer new payment options to their customers, to ensure that credit card holders don’t seek alternatives. Providing outstanding service and incentivizing engagement through loyalty programs helps maintain a solid and ongoing relationship with customers. Encouraging frequent card usage with a loyalty program will lead to increased overall revenue and keep the brand on top of customers’ minds.

Here are a few ideas on how to encourage customers to keep using their credit cards with the help of a loyalty program:

- Offer 1% cashback on all purchases

- Provide points for every dollar spent, which can be exchanged for rewards of the customer’s choosing

- Offer an instant reward when customers make a purchase or allow points to be spent on rewards immediately after transactions

- Bonus-point promotions targeted to specific transaction types

- Develop seasonal promotions for bonus points

- Encourage spend in categories which are not typically covered by BNPL, such as fuel

- In order to make customers feel special, send branded messages and thank you letters for using your card

Antavo’s budget planning ebook can help plan your rewards system and make every penny count.

The Final Judgement on Buy Now, Pay Later

Rapid shifts in customer behavior and the continued rise of online shopping have fueled BNPL’s popularity. Buy now, pay later makes it easier to break down the price, so customers don’t have to use their entire paycheck or savings at once. It is a little bit like having a credit card without having to go through intensive credit checks.

Of course, there is a downside to this system, too. It might be worrying that this painless borrowing-with-a-click is the “gamification” of shopping, and creates the sense that spending isn’t real. Also, it may lead to customers taking out credit in situations where they simply would have refrained from making the purchase altogether. The fact that customers can get a short-term loan to buy just about anything, anywhere encourages shoppers to purchase more than they had originally intended.

Implementing a loyalty program, in which companies offering buy now, pay later services, reward paying on time is an excellent way to motivate responsible spending. The rising popularity of BNPL also affects financial institutions. By launching a rewards program, these institutions can incentivize the ongoing use of credit cards to make sure customers don’t leave the more traditional payment method behind.

If you want to know more about how our technology can make your loyalty program concept come to life, book a demo or include us in your RFP.

In the meantime, download our worksheet to make planning your future loyalty program smoother.

Barbara Kekes-Szabo Barbara Kekes-Szabo LinkedIn profile

Barbara is a Loyalty Program Specialist at Antavo and a Certified Loyalty Marketing Professional - CLMP. She is also a writing expert with several years of experience in marketing and also in the information technology industry. In her free time she likes traveling the world, reading crime stories, and doing crossword puzzles.